Minimum Car Insurance Coverage: Is It Enough?

Many of us probably assume that car insurance is a no brainer. If a driver is insured and causes an accident, their car insurance should cover all the related expenses. Right? Not necessarily. In Missouri, the minimum amount of car insurance required by law is only $25,000. How many days in the hospital would $25,000 cover? Not many.

Missouri’s Motor Vehicle Financial Responsibility Law is RSMo 303.190. It requires the following coverage: $25,000 in liability coverage per person up to $50,000 per incident and $10,000 for property damage. What does this mean? If you have a relative new car and spend more than a day or two in the hospital, there won’t be nearly enough insurance proceeds to cover your injuries and damage.

Missouri’s minimum insurance limits used to be lower. In 1981, the limit was raised from $10,000 per person to $25,000. But it’s stayed there ever since. Think about what’s happened to prices and inflation since 1981.

A loaf of bread was $0.53 in 1981. Now it’s $1.41. Campbell’s soup was 5 for a dollar in 1981. Now it’s $1.09 per can. In 1981, a package of Oreo’s sold for $1.69. Today, they’re $4.49.

Using the consumer price index (CPI), $25,000 in 1981 is the equivalent to more than $65,000 today. The minimum insurance limits provide less than half of the protection they did when they were first enacted. And the level of protection is going down every year.

If you look just at medical costs, it becomes much worse because the cost of medical care has increased much faster than the CPI. It would take $131,000 of insurance coverage to provide the same level of medical care as the $25,000 limits provided in 1981. In Missouri, we have less than 1/5 of the protection for bodily injury as we had in 1981.

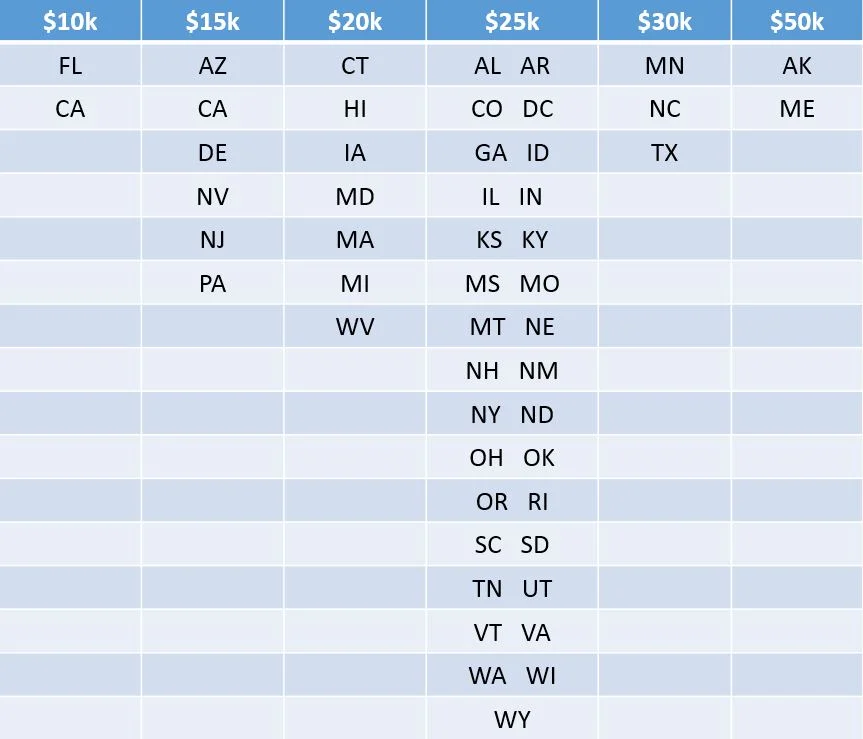

Sadly, Missouri’s minimum limits remain squarely within the majority of state minimum auto coverage. Only 5 states require greater coverage and 15 states have lower coverage requirements.

What can you do to protect yourself if you become injured by a diver with only minimum (or even no) auto insurance coverage? There are several options (and you should choose at least some form of each!):

Maintain adequate medical/health insurance. Whether you have a simple cold or are injured by a negligent driver, your health insurance should cover your injuries. The better health insurance you have, the better protected you are in the event of an injury. In some states and under some employer-sponsored health plans, however, you must reimburse your health insurance provider if there turns out to be insurance or other other payment from the negligent driver.

Increase your minimum uninsured motorist coverage. Like mandatory minimum auto coverage, there are is also equivalent mandatory minimum uninsured motorist coverage (UM coverage). These minimums ensure you are protected at least to the minimum level of coverage required by your state. But as detailed above, these minimums are unlikely to be sufficient to cover your medical and other financial needs if you suffer more than minimal injury in a collision. Talk to your insurance agent about increasing your coverage for uninsured motorist coverage above the minimum amount.

Purchase underinsured motorist coverage. Underinsured motorist coverage is additional insurance you purchase which is applied to increase the coverage for a negligent driver who injures you or your property. The practical application of underinsured motorist coverage (UIM coverage) will vary depending on the specific language of the policy and requirements of particular states.

In some circumstances, the UIM is straightforward. If you have purchased $100,000 of UIM coverage and the negligent driver carries minimum $25,000 coverage; then your UIM “stacks” and you will have a total combined limit of $125,000 in available coverage.

In other circumstances, the UIM acts to simply increase the negligent driver’s insurance to the UIM coverage amount. In this situation, a $100,000 UIM policy would only provide an additional $75,000 in coverage if the negligent driver carried minimum coverage of $25,000. Your total protection would be the face amount of the UIM policy.

You should ask your insurance agent to fully explain to you how your particular UIM coverage will work. In any event, UIM is typically an affordable way to ensure a greater level of protect in the even you are injured by a negligent driver.

As medical expenses continue their rapid, ever-higher expansion, it’s time for states to consider increasing mandatory minimum coverage for motorists. In the meantime, be sure that you and your family are protected by purchasing adequate, health, UM, and UIM coverage.

Location

Northland Injury Law

4151 N. Mulberry Drive

Suite 225

Kansas City, MO 64116

© 2025 Northland Injury Law • All Rights Reserved •

Digital Marketing By ![]()